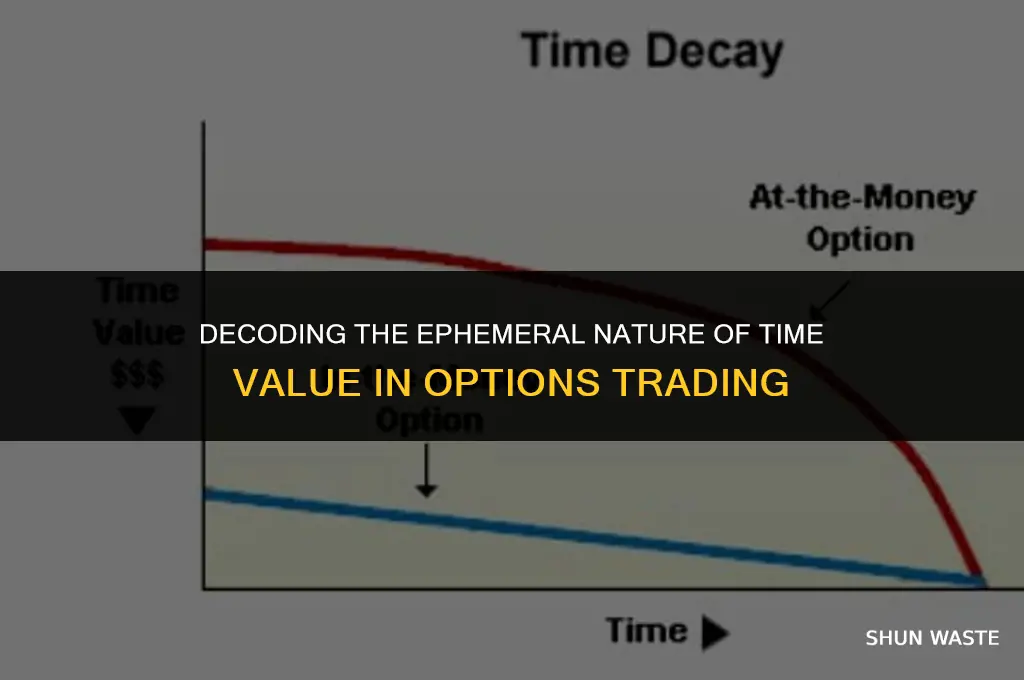

The time value of an option is a critical component in options trading, representing the premium paid for the flexibility to buy or sell an underlying asset at a predetermined price before a specific expiration date. However, this time value is inherently a wasting asset, meaning it decreases over time. This decay is due to the diminishing probability of the option being exercised as the expiration date approaches. Essentially, the closer the option is to expiring, the less valuable its time component becomes, as there is less time for the underlying asset's price to move favorably. This concept is fundamental for traders to understand, as it impacts the pricing and strategy of options contracts.

Explore related products

$3.99 $12.97

What You'll Learn

- Decay Over Time: Options lose value as time passes due to decreased flexibility and market changes

- Impact of Volatility: Higher volatility increases the chance of the option being in-the-money, affecting its time value

- Interest Rates Influence: Rising interest rates can reduce the present value of future cash flows, impacting time value

- Exercise Limitation: Options can only be exercised at specific times, limiting their utility and value over time

- Opportunity Cost: Holding an option means forgoing other investment opportunities, which can reduce its overall value

![]()

Decay Over Time: Options lose value as time passes due to decreased flexibility and market changes

Options, by their very nature, are time-sensitive financial instruments. As time progresses, the value of an option can significantly diminish, a phenomenon known as time decay. This decay is a result of the decreasing flexibility that comes with holding an option. When an investor buys an option, they gain the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (strike price) before a certain date (expiration date). However, as the expiration date approaches, the investor's ability to benefit from price movements in the underlying asset decreases, leading to a loss in the option's value.

Market changes also play a crucial role in the decay of an option's value over time. Volatility, interest rates, and dividends can all impact the price of an option. For instance, if the market becomes less volatile, the value of an option may decrease because there is less potential for significant price movements in the underlying asset. Similarly, if interest rates rise, the cost of holding an option increases, which can lead to a decrease in its value. Dividends paid by the underlying asset can also reduce the value of an option, as they decrease the asset's price and, consequently, the option's potential payoff.

The concept of time decay is particularly relevant for investors who use options as part of their trading strategies. For example, an investor who buys a call option with a strike price of $50 and an expiration date of one month may expect the underlying asset's price to rise above $50 within that time frame. However, if the asset's price remains below $50 as the expiration date approaches, the option's value will decay, potentially resulting in a loss for the investor. This highlights the importance of understanding and managing the risks associated with time decay when trading options.

To mitigate the effects of time decay, investors can employ various strategies. One approach is to buy options with longer expiration dates, which provides more time for the underlying asset's price to move in the desired direction. Another strategy is to sell options, which can generate income through premiums received. However, selling options also comes with its own set of risks, as the seller is obligated to fulfill the terms of the option if the buyer chooses to exercise it. Therefore, a thorough understanding of the underlying asset, market conditions, and the implications of time decay is essential for successful options trading.

In conclusion, the decay of an option's value over time is a complex process influenced by a variety of factors, including the option's expiration date, market volatility, interest rates, and dividends. Investors who trade options must be aware of these factors and develop strategies to manage the risks associated with time decay. By doing so, they can potentially maximize their returns while minimizing their losses in the dynamic world of options trading.

Overcoming Procrastination: Strategies to Maximize Your Time

You may want to see also

Explore related products

![]()

Impact of Volatility: Higher volatility increases the chance of the option being in-the-money, affecting its time value

The impact of volatility on the time value of an option is a critical aspect to understand in the realm of options trading. Volatility, in this context, refers to the rate at which the price of the underlying asset fluctuates. Higher volatility implies greater uncertainty and risk, which can significantly influence the value of an option.

When volatility increases, the probability of the option being in-the-money (ITM) also rises. This is because higher volatility means larger price swings, increasing the likelihood that the asset's price will move beyond the option's strike price. As a result, the option's intrinsic value, which is the difference between the asset's price and the strike price, becomes more substantial.

However, the relationship between volatility and time value is not straightforward. While higher volatility can increase the chance of the option being ITM, it also affects the time value of the option. Time value represents the premium paid for the potential future price movements of the underlying asset. In a high-volatility environment, the time value of an option may decrease more rapidly due to the increased risk and uncertainty.

This phenomenon can be observed in the Black-Scholes model, a widely used framework for pricing options. According to this model, the time value of an option is influenced by several factors, including the time to expiration, the strike price, the risk-free interest rate, and the volatility of the underlying asset. As volatility increases, the time value component of the option price may decline, even if the intrinsic value rises.

In practical terms, this means that options traders must carefully consider the impact of volatility on their positions. While higher volatility can present opportunities for greater profits, it also increases the risk of losses. Traders must balance the potential benefits of increased volatility against the potential drawbacks, taking into account the time value of their options and how it may be affected by market conditions.

In conclusion, the impact of volatility on the time value of an option is a complex and multifaceted issue. Understanding this relationship is essential for options traders, as it can significantly influence their trading strategies and risk management decisions. By recognizing how volatility affects both the intrinsic and time values of an option, traders can make more informed and effective choices in the dynamic world of options trading.

Stop Wasting Time Changing Voices: Embrace Your Unique Sound

You may want to see also

Explore related products

$126 $156.95

![]()

Interest Rates Influence: Rising interest rates can reduce the present value of future cash flows, impacting time value

Rising interest rates can significantly impact the present value of future cash flows, which is a critical component in determining the time value of an option. The time value of an option is essentially the premium paid for the flexibility to buy or sell an underlying asset at a predetermined price (strike price) within a specific timeframe. This flexibility is valuable because it allows the option holder to benefit from potential price movements in the underlying asset without the obligation to actually purchase or sell it.

However, when interest rates rise, the present value of future cash flows decreases. This is because the higher interest rate provides an alternative investment opportunity that yields a higher return with less risk. As a result, investors may be less willing to pay a premium for the flexibility offered by options, leading to a decrease in the time value of the option.

To illustrate this concept, consider an example where an investor is evaluating a call option on a stock with a strike price of $50 and an expiration date of one year. If the current stock price is $45 and the risk-free interest rate is 5%, the present value of the potential cash flow from exercising the option (assuming the stock price rises to $60 at expiration) would be lower than if the interest rate were 3%. This is because the higher interest rate of 5% provides a better return on investment compared to the potential gain from exercising the option.

Furthermore, the impact of rising interest rates on the time value of an option is more pronounced for options with longer expiration dates. This is because the present value of future cash flows is discounted over a longer period, resulting in a greater reduction in value. Conversely, options with shorter expiration dates are less affected by changes in interest rates, as the time value is primarily driven by the volatility of the underlying asset and the proximity to expiration.

In conclusion, rising interest rates can reduce the present value of future cash flows, thereby impacting the time value of an option. This effect is more significant for options with longer expiration dates and can influence an investor's decision to purchase or sell options. Understanding the relationship between interest rates and the time value of an option is crucial for making informed investment decisions in the options market.

Reevaluating Leisure: Why Holidays Might Not Be Worth the Hype

You may want to see also

Explore related products

$16.99 $11.46

$87.85 $111.95

![]()

Exercise Limitation: Options can only be exercised at specific times, limiting their utility and value over time

Options, by their very nature, are time-sensitive financial instruments. One of the key limitations of options is that they can only be exercised at specific times, which significantly impacts their utility and value over time. This exercise limitation is a critical factor in understanding why the time value of an option is considered a wasting asset.

To illustrate this concept, consider a scenario where an investor purchases a call option on a stock with a strike price of $50, expiring in three months. If the stock price rises to $60 within the first month, the option becomes profitable. However, if the investor is unable to exercise the option until the three-month expiration date, they may miss out on potential gains if the stock price were to drop before then. This limitation on when the option can be exercised inherently reduces its value and utility, as the investor is unable to capitalize on favorable market conditions that may arise before the expiration date.

Furthermore, the exercise limitation can also lead to a decrease in the option's value over time, even if the underlying stock price remains stable or increases. This is because the option's value is not only dependent on the stock price but also on the remaining time to expiration. As the expiration date approaches, the option's value will decrease, regardless of the stock price, due to the reduced flexibility and time available for exercise.

In addition to the direct impact on value and utility, the exercise limitation can also influence an investor's decision-making process. For instance, an investor may be more inclined to hold onto an option that is close to expiration, hoping for a favorable price movement, rather than exercising it prematurely and potentially missing out on greater gains. This behavioral aspect can lead to suboptimal investment decisions and further underscores the importance of understanding the exercise limitation in options trading.

In conclusion, the exercise limitation of options is a crucial factor that contributes to the time value of an option being considered a wasting asset. This limitation not only affects the option's value and utility over time but also influences investor behavior and decision-making. By recognizing and understanding this limitation, investors can better navigate the complexities of options trading and make more informed investment choices.

The Art of Procrastination: Why We Waste Time Looking Around

You may want to see also

Explore related products

![]()

Opportunity Cost: Holding an option means forgoing other investment opportunities, which can reduce its overall value

Holding an option comes with an inherent opportunity cost, as it means forgoing other potential investment opportunities. This cost can significantly reduce the overall value of the option over time. For instance, if an investor holds a call option on a stock, they may miss out on the opportunity to invest in other stocks or assets that could have yielded higher returns. This opportunity cost is a key factor in why the time value of an option is considered a wasting asset.

The opportunity cost of holding an option can be particularly high in volatile markets, where the potential for gains (or losses) is greater. In such scenarios, the value of the option may decrease more rapidly due to the increased likelihood of missing out on more lucrative investments. This highlights the importance of considering the opportunity cost when deciding whether to hold an option, as it can have a significant impact on the investor's overall portfolio performance.

Furthermore, the opportunity cost of holding an option can also be influenced by the investor's risk tolerance and investment goals. For example, a risk-averse investor may be more willing to hold an option as a form of insurance against potential losses, even if it means forgoing other investment opportunities. On the other hand, a risk-seeking investor may be more likely to let the option expire in order to pursue higher-risk, higher-reward investments.

In conclusion, the opportunity cost of holding an option is a critical factor to consider when evaluating the time value of an option. By understanding the potential impact of forgoing other investment opportunities, investors can make more informed decisions about whether to hold or let go of an option, ultimately maximizing their portfolio's overall value.

Debunking the Myth: Why Ab Workouts Might Not Be Worth Your Time

You may want to see also

Frequently asked questions

The time value of an option refers to the portion of the option's premium that is attributable to the passage of time. It is considered a wasting asset because it decreases in value as time passes, eventually expiring worthless if not exercised before the option's expiration date.

The time value of an option decreases over time because the uncertainty about the future price of the underlying asset decreases as the expiration date approaches. This reduction in uncertainty reduces the potential for profit from holding the option, thus decreasing its value.

The time decay of an option affects its pricing by reducing the overall value of the option as the expiration date nears. This is reflected in the option's premium, which will decrease over time, all else being equal. Traders must consider this time decay when pricing and trading options to ensure they are making informed decisions.

Yes, the time value of an option can increase before expiration if there is a significant change in the volatility of the underlying asset or if the market's expectations about the future price of the asset shift dramatically. However, this increase is typically offset by the continuous decay of time value over time.

Traders can manage the risk associated with the time decay of options by employing various strategies, such as:

- Buying options with longer expiration dates to allow more time for the trade to develop.

- Selling options with shorter expiration dates to capitalize on the rapid time decay.

- Rolling options positions to extend the expiration date and maintain exposure to the underlying asset.

- Hedging options positions with other financial instruments to mitigate potential losses due to time decay.