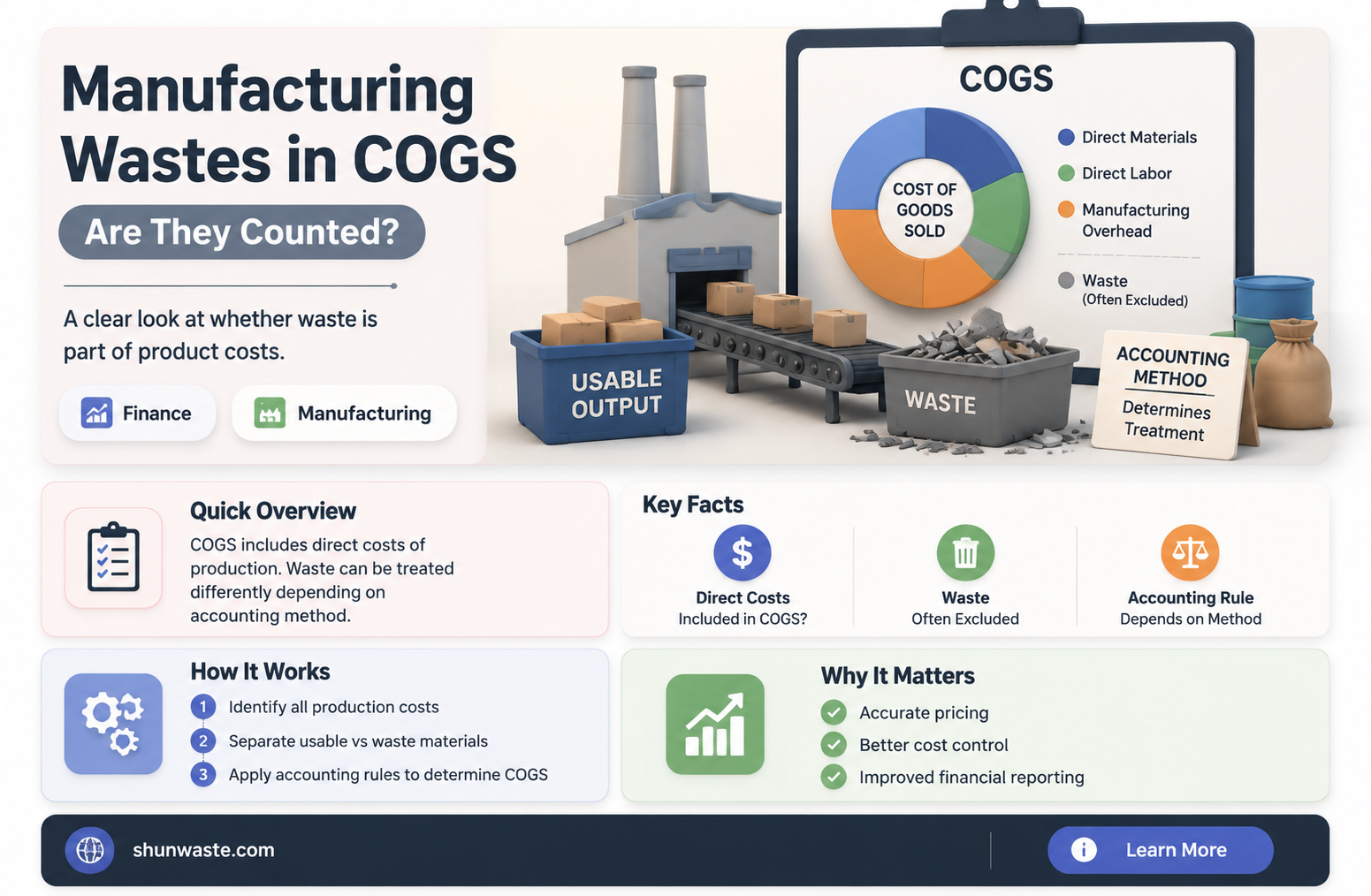

Manufacturing wastes, which include scrap materials, defective products, and by-products generated during the production process, are a critical aspect of cost accounting and financial analysis. The question of whether these wastes should be considered part of the Cost of Goods Sold (COGS) is a topic of debate among accountants and financial professionals. On one hand, including manufacturing wastes in COGS reflects the true cost of production, as these wastes are an inherent part of the manufacturing process and contribute to the overall expenses incurred to produce goods. On the other hand, some argue that only the costs directly associated with the finished products should be included in COGS, while wastes should be treated as separate expenses or losses. Understanding the treatment of manufacturing wastes in COGS is essential for accurate financial reporting, cost control, and decision-making in manufacturing businesses.

Explore related products

What You'll Learn

![]()

Definition of COGS and Waste Inclusion

Cost of Goods Sold (COGS) is a critical metric in financial accounting, representing the direct costs attributable to the production of goods sold by a company. It includes expenses such as raw materials, direct labor, and manufacturing overhead. However, the inclusion of manufacturing waste within COGS is a nuanced issue that requires careful consideration. Waste can arise from various sources, including defective units, scrap materials, and inefficiencies in the production process. While some waste is inevitable, distinguishing between normal and abnormal waste is essential for accurate financial reporting.

Analytically, normal waste refers to the unavoidable byproducts of manufacturing processes, such as trimmings in textile production or excess material in machining. These costs are typically included in COGS because they are directly tied to the production of salable goods. For example, a furniture manufacturer might account for wood scraps as part of the cost of producing tables and chairs. Abnormal waste, on the other hand, results from inefficiencies, errors, or suboptimal processes and is generally excluded from COGS. An instance of this could be a batch of products ruined due to machine malfunction, which would be treated as a separate expense.

From an instructive perspective, companies must establish clear criteria for classifying waste to ensure compliance with accounting standards. The Financial Accounting Standards Board (FASB) and International Financial Reporting Standards (IFRS) provide guidelines, but interpretation can vary. A practical tip is to document the nature and cause of waste, linking it to specific production activities. For instance, if a pharmaceutical company produces 10,000 units but 500 are discarded due to contamination, the cost of the 500 units should be analyzed to determine if it qualifies as normal or abnormal waste.

Persuasively, including manufacturing waste in COGS can impact a company’s financial statements and tax obligations. Proper classification ensures that gross profit margins are accurately reflected, providing stakeholders with a true picture of operational efficiency. Misclassification, however, can lead to distorted financial ratios and misinformed decision-making. For example, a company that incorrectly excludes normal waste from COGS might appear more profitable than it actually is, potentially misleading investors.

Comparatively, industries handle waste inclusion differently based on their production processes. In food manufacturing, spoilage is often considered normal waste and included in COGS, whereas in electronics, defective components might be treated as abnormal waste depending on the defect rate. A descriptive example is the automotive industry, where metal scraps from stamping processes are typically absorbed into COGS, while vehicles damaged during assembly are often written off as separate losses. Understanding these industry-specific practices is crucial for accurate financial reporting.

In conclusion, the inclusion of manufacturing waste in COGS depends on whether it is classified as normal or abnormal. Companies must adopt a systematic approach to waste classification, ensuring alignment with accounting standards and industry norms. By doing so, they can maintain transparency, accuracy, and reliability in their financial statements, ultimately fostering trust among stakeholders.

Human Waste Production: Transforming Ecosystems with Unintended Consequences

You may want to see also

Explore related products

![]()

Types of Manufacturing Wastes in COGS

Manufacturing wastes are indeed a critical component of Cost of Goods Sold (COGS), but not all wastes are treated equally in financial reporting. Understanding the types of manufacturing wastes and their categorization within COGS is essential for accurate cost accounting and operational efficiency. Here’s a breakdown of the key waste types and their implications.

Direct vs. Indirect Wastes: A Categorization Challenge

Manufacturing wastes fall into two broad categories: direct and indirect. *Direct wastes*, such as scrap materials from production runs, are often traceable to specific products and are typically included in COGS. For example, if a furniture manufacturer discards 5% of wood due to defects, this cost is directly allocated to the product’s COGS. In contrast, *indirect wastes*, like excess energy consumption or overproduction, are usually absorbed into overhead costs and allocated across multiple products. However, if indirect wastes are significant and identifiable, they may be partially included in COGS, depending on accounting standards and materiality thresholds.

Normal vs. Abnormal Spoilage: The Thin Line in COGS

Spoilage in manufacturing is classified as either normal or abnormal, each with distinct COGS treatment. *Normal spoilage*, an inevitable outcome of production processes, is included in COGS. For instance, a bakery might expect 2% of bread loaves to spoil during baking, and this cost is factored into the product’s COGS. Conversely, *abnormal spoilage*, caused by inefficiencies or errors, is excluded from COGS and treated as a loss. If a machine malfunction ruins 10% of a batch, this excess spoilage is expensed separately, not buried in COGS.

Rework and Scrap: Hidden Costs in Production

Rework and scrap are tangible wastes that directly impact COGS. *Rework* occurs when defective units are repaired and reintroduced into production, incurring additional labor and material costs. These costs are added to COGS, inflating the per-unit cost. *Scrap*, on the other hand, refers to unusable materials with residual value. For example, a metal fabrication plant might sell scrap metal at 10% of its original cost, deducting this recovery from COGS. Proper tracking of rework and scrap is crucial for maintaining cost accuracy and identifying process inefficiencies.

Overproduction and Inventory Obsolescence: The Silent Wastes

Overproduction and inventory obsolescence are less visible but equally damaging wastes. *Overproduction* ties up capital in excess inventory, increasing holding costs and storage expenses. While these costs are not directly included in COGS, they inflate the overall cost structure, indirectly affecting profitability. *Inventory obsolescence*, such as outdated electronics components, is written down as a loss, reducing reported COGS. Companies must balance production schedules and demand forecasts to minimize these wastes and maintain lean operations.

Practical Takeaway: Optimize Waste Management to Control COGS

To effectively manage manufacturing wastes within COGS, businesses should implement robust tracking systems, differentiate between waste types, and align accounting practices with industry standards. Regular audits of production processes can identify inefficiencies, while lean manufacturing principles can reduce waste at the source. By treating wastes as actionable data points, companies can lower COGS, improve margins, and enhance overall financial health.

Sewage Waste's Devastating Environmental Impact: Causes, Effects, and Solutions

You may want to see also

Explore related products

$84.67 $158

![]()

Accounting Standards for Waste Costs

Manufacturing waste, whether from spoilage, scrap, or inefficiencies, directly impacts a company’s cost of goods sold (COGS). Accounting standards require these costs to be treated consistently to ensure financial statements reflect true production expenses. Under both GAAP and IFRS, normal waste—inevitable losses inherent to production—is capitalized as part of inventory and COGS. For example, a bakery’s dough trimmings are considered normal waste and included in the cost of bread production. Abnormal waste, such as losses from machine malfunctions, is expensed immediately as a period cost, not included in COGS, to avoid distorting inventory valuation.

To allocate waste costs accurately, companies must first classify waste as normal or abnormal. Normal waste is allocated based on historical data or industry benchmarks. For instance, a textile manufacturer might allocate 5% of raw material costs to normal waste. This allocation ensures COGS reflects the true cost of production. Abnormal waste requires separate tracking and immediate expensing. For example, a batch ruined due to a supplier’s defective material would be expensed as a loss, not included in COGS. Proper classification prevents overstatement of inventory and ensures profitability metrics remain reliable.

Transparency in waste cost reporting is critical for stakeholders. Companies must disclose their waste classification methods and allocation criteria in financial notes. This clarity helps investors and analysts assess operational efficiency and cost management. For instance, a company with consistently high abnormal waste may signal poor quality control or outdated machinery. Conversely, low waste costs relative to industry peers can indicate superior process management. Standardized reporting ensures comparability across companies and industries, fostering trust in financial statements.

Finally, integrating waste cost management into ERP or accounting systems streamlines compliance with accounting standards. Automated tracking of waste quantities and costs reduces errors and ensures consistent application of policies. For example, a manufacturing firm might use IoT sensors to monitor scrap rates in real-time, linking data directly to COGS calculations. Such technology not only enhances accuracy but also provides actionable insights for reducing waste. By treating waste costs as a strategic component of COGS, companies can improve financial health and operational efficiency simultaneously.

Cerebral Salt Wasting: Unraveling Its Role in Causing Cerebral Edema

You may want to see also

Explore related products

![]()

Impact of Waste on COGS Calculation

Manufacturing waste directly inflates Cost of Goods Sold (COGS) by embedding inefficiencies into production costs. Raw material scrap, defective units, and overproduction all represent resources consumed but not converted into salable products. For example, a factory producing 1,000 units with 10% scrap uses materials for 1,100 units but only invoices 1,000. The wasted 100 units’ material cost still enters COGS, diluting gross profit margins. This hidden cost often escapes attention because it’s absorbed into inventory valuation rather than tracked as a separate expense.

Consider a textile manufacturer incurring 15% fabric waste due to cutting inefficiencies. If fabric costs $5 per yard and 10,000 yards are purchased, $7,500 (1,500 wasted yards × $5) becomes embedded in COGS despite not contributing to finished goods. This scenario underscores why waste reduction initiatives—such as precision cutting technology or pattern optimization—aren’t just operational improvements but financial imperatives. Every percentage point of waste reduction lowers COGS proportionally, enhancing profitability without increasing sales.

The impact of waste on COGS calculation extends beyond direct materials. Labor hours spent on defective units, machine downtime from equipment malfunctions, and energy consumption for rework all inflate production costs. For instance, a machine operator earning $20/hour who spends 2 hours daily repairing defects adds $40 to daily COGS without producing additional value. Such indirect waste often lacks traceability in traditional accounting systems, making it critical to implement activity-based costing (ABC) to allocate these costs accurately.

A comparative analysis of two electronics manufacturers illustrates this point. Company A, with a 5% defect rate, reports COGS of $1.2 million on $2 million revenue (60% COGS ratio). Company B, achieving 2% defects through lean practices, reports $1 million COGS on the same revenue (50% ratio). Despite identical sales, Company B’s gross profit is $400,000 higher solely due to waste control. This example highlights how waste management isn’t merely an operational metric but a strategic lever for financial performance.

To mitigate waste’s impact on COGS, manufacturers should adopt a three-step approach: measure, allocate, and optimize. First, quantify waste by category (material, labor, energy) using real-time data from IoT sensors or ERP systems. Second, allocate these costs to specific products or processes via ABC to identify high-impact areas. Third, implement targeted interventions—such as just-in-time inventory, predictive maintenance, or employee training—to reduce waste at its source. By treating waste as a variable cost rather than an inevitability, companies can systematically lower COGS and improve competitive positioning.

Waste Management in Paramecium: Understanding Their Unique Excretion Process

You may want to see also

Explore related products

![]()

Strategies to Minimize Waste in COGS

Manufacturing waste directly inflates Cost of Goods Sold (COGS), eroding profitability and sustainability. Every scrap of unused material, machine downtime, and defective product represents lost revenue. Minimizing this waste isn’t just about cost-cutting—it’s about optimizing operations for long-term viability.

Identify Waste Streams with Precision

Begin by mapping your manufacturing process to pinpoint where waste occurs. Use tools like value stream mapping or lean manufacturing principles to categorize waste into types: overproduction, waiting time, defects, excess inventory, unnecessary motion, over-processing, and transportation. For instance, a textile manufacturer might discover that 15% of fabric is wasted due to inefficient cutting patterns. Analyzing these streams provides a baseline for targeted reduction strategies.

Implement Just-in-Time (JIT) Inventory Management

JIT minimizes excess inventory by aligning production with demand. For a food processing plant, this could mean ordering raw materials in smaller batches to reduce spoilage. Pair JIT with real-time demand forecasting tools to avoid overproduction. Caution: JIT requires reliable suppliers and robust logistics to prevent stockouts.

Invest in Technology for Precision and Efficiency

Adopting technologies like IoT sensors, automation, and AI can drastically reduce waste. For example, a metal fabrication company might use laser cutting machines to reduce material waste by 20%. Predictive maintenance tools can also minimize machine downtime, ensuring continuous production. While the upfront cost is high, the ROI comes from reduced scrap and increased output.

Engage Employees in Continuous Improvement

Empower workers to identify and address inefficiencies. Implement a suggestion system where employees propose waste-reducing ideas, such as reusing scrap materials or optimizing workstation layouts. For instance, a furniture manufacturer might repurpose wood scraps into smaller products like coasters. Incentivize participation through bonuses or recognition programs to foster a culture of efficiency.

Measure and Iterate

Track waste reduction metrics regularly to gauge progress. Use key performance indicators (KPIs) like scrap rate, machine utilization, and cycle time. For a chemical plant, reducing waste by 10% could save $50,000 annually. Adjust strategies based on data—what works in one area might not apply elsewhere. Continuous monitoring ensures that waste minimization remains a dynamic, ongoing process.

By systematically addressing waste in COGS, businesses can enhance profitability, reduce environmental impact, and build resilience in an increasingly competitive market.

How Blood Transports and Eliminates Waste in the Body

You may want to see also

Frequently asked questions

Yes, manufacturing wastes, such as scrap materials and spoilage, are typically included in COGS if they are a normal and expected part of the production process.

Abnormal manufacturing wastes, which are unexpected or excessive, are usually excluded from COGS and treated as a separate expense on the income statement.

No, only direct manufacturing wastes tied to the production process are included in COGS, while indirect or administrative wastes are treated as operating expenses.

Yes, normal manufacturing wastes can generally be deducted as part of COGS for tax purposes, as they are considered a cost of producing goods for sale.